URR 725 are the Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits. These rules are published by the International Chamber of Commerce (ICC). The Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits will apply to any bank-to-bank reimbursement only when the text of the reimbursement authorization expressly indicates that is is subject to these rules.

If a credit involves bank-to-bank reimbursement and the credit does not state that the reimbursement is subject to URR 725, then Article 13 (b) and 13 (c) will apply for that reimbursement arrangement.

Table of Contents

URR Latest Version – URR 725

URR 725 is the latest version of the Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits. It came into effect from 1st October 2008.

History of URR

The URR was first published in the year 1995 under the title URR 525,

The revised version of URR was published in the year 2008 under the title URR 725. (ICC Publication No. 725)

URR 725 Articles

There are 17 articles in URR 725. They are classified into four groups as given below:

General Provisions and Definitions

- Application of URR

- Definitions

- Reimbursement Authorizations Versus Credits

Liabilities and Responsibilities

- Honour of a Reimbursement Claim

- Responsibility of the Issuing Bank

Form and Notification of Authorizations, Amendments and Claims

- Issuance and Receipt of a Reimbursement Authorization or Reimbursement Amendment

- Expiry of a Reimbursement Authorization

- Amendment or Cancellation of a Reimbursement Authorization

- Reimbursement Undertaking

- Standards for a Reimbursement Claim

- Processing a Reimbursement Claim

- Duplication of a Reimbursement Authorization

Miscellaneous Provisions

- Foreign Laws and Usages

- Disclaimer on the Transmission of Messages

- Force Majeure

- Charges

- Interest Claims/Loss of Value

URR 725 important terms

In this section we’ll discuss some important terms and definitions related to URR 725. Whenever a SWIFT message type is involved, the relevant SWIFT message type is mentioned inside brackets.

Issuing Bank: Issuing bank is the bank which issues both the letter of credit (MT700) and the reimbursement authorization (MT740).

Reimbursing Bank: Reimbursing bank is the bank which reimburses the claiming bank upon receipt of their claim (MT742). It is the issuing bank who provides instructions or authorization to the reimbursing bank to reimburse the claiming bank.

Claiming Bank: Claiming bank is the bank which claims reimbursement from a reimbursing bank. It is that bank which honours or negotiates a credit and instead of claiming the funds from issuing bank, claims the same from a reimbursing bank. This arrangement is already decided at the time of issuance of the letter of credit.

Reimbursement authorization: Reimbursement authorization (MT740) is an instruction or authorization issued by an issuing bank to a reimbursing bank to reimburse a claiming bank. The reimbursement authorization is independent of the credit.

Reimbursement authorization amendment: Reimbursement authorization amendment (MT747) is a message issued by an issuing bank to a reimbursing bank to amend the terms of a reimbursement authorization.

Reimbursement Claim: Reimbursement claim (MT742) is a request for reimbursement sent by the claiming bank to the reimbursing bank.

Reimbursement Undertaking: Reimbursement undertaking is a separate irrevocable undertaking issued by the reimbursing bank to the claiming bank stating that the reimbursing bank will honour the claiming bank’s reimbursement claim provided they comply with the terms and conditions of the reimbursement undertaking. It is issued upon the authorization or request of the issuing bank.

Important points about Reimbursement Authorization as per URR 725

- A reimbursement authorization should expressly state that it is subject to URR 725.

- A reimbursement authorization is independent of the letter of credit to which it refers and the reimbursing bank is not bound by the terms and conditions of the credit.

- In the reimbursement authorization, an issuing bank should not provide any requirement of a certificate of compliance with the terms and conditions of the credit, to be submitted by the claiming bank along with its reimbursement claim.

- A reimbursement authorization must state the below fields in the message:

- Letter of credit number

- Currency and amount

- Additional amounts payable and tolerance, if any

- Specific Claiming Bank, or whether any bank can claim

- Parties responsible for claiming bank’s and reimbursing bank’s charges i.e. whether the applicant or the beneficiary will pay these charges.

- A reimbursement authorization should not be subject to an expiry date or a latest date for presentation of a claim, unless this is expressly agreed to by the reimbursing bank.

- Requirement for a pre-debit notification (from the reimbursing bank to the issuing bank) should be included in the reimbursement authorisation. This requirement should also be included in the letter of credit.

What is a pre-debit notification?

A pre-debit notification is a message sent by the reimbursing bank to the issuing bank. Its purpose is to inform the issuing bank in advance regarding a debit to be posted to their account for a claim received from a claiming bank.

A pre-debit notification period is specified in number of banking days. An important point to be noted here is that a reimbursing bank has a maximum of 3 banking days following the day of receipt of a reimbursement claim to process the claim. If a pre-debit notification is required by the issuing bank, then this pre-debit notification period will be in addition to the processing period of 3 banking days mentioned above. Let’s say, there is a pre-debit notification period of 3 banking days specified in the letter of credit. Then the reimbursing bank will have a total of 6 banking days to honour the claim – 3 banking days towards pre-debit notification period and 3 banking days towards it processing period.

Requirement of a pre-debit notification should be included by the issuing bank in both the reimbursement authorization and the letter of credit.

What is pre-notification of a reimbursement claim?

A pre-notification of a reimbursement claim is a message sent by the claiming bank to the issuing bank. Its purpose is to inform the issuing bank in advance that the claiming bank is going to claim the funds from the reimbursing bank on a specified date.

A pre-notification period is specified in number of banking days. Let’s say, there is a pre-notification period of 3 banking days specified in the letter of credit. Then the claiming bank has to send pre-notification of a reimbursement claim to the issuing bank 3 banking days before the date on which they will claim reimbursement from the reimbursing bank.

Requirement of a pre-notification of a reimbursement claim must be included by the issuing bank in the letter of credit and not in the reimbursement authorization.

Processing of a Reimbursement Claim under URR 725

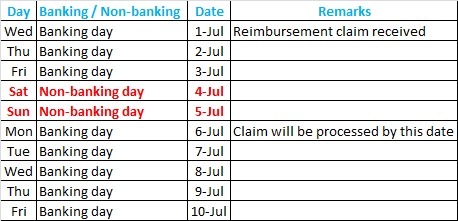

We recall that a reimbursing bank has a maximum of 3 banking days following the day or receipt of the reimbursement claim to process the claim. We’ll discuss a few situations with examples. Please refer to the calendar in the image while going through the examples.

Situation 1: No requirement of Pre-debit notification

Let’s assume the claiming bank has presented the reimbursement claim to the reimbursing bank on 1st July.

The claim will processed within a maximum of 3 banking days following the day of receipt of claim i.e. 1st July. 6th July is the 3rd banking day following the day of receipt of claim. Saturday and Sunday are excluded being non-banking days.

So the claim will be processed within 6th July.

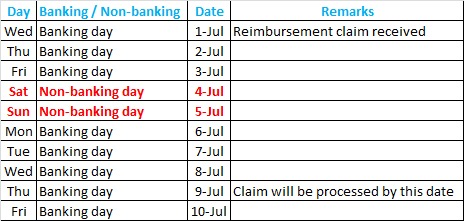

Situation 2: Requirement of Pre-debit notification

In the same example as above, let’s assume that there is a requirement of pre-debit notification period of 3 banking days. The claiming bank has presented the reimbursement claim to the reimbursing bank on 1st July.

On receipt of the claim, the reimbursing bank will send pre-debit notification to the issuing bank. The pre-debit notification period of 3 days is in addition to the processing period of 3 days required for the reimbursing bank to process the claim. The processing period will start after the end of pre-debit notification period. So the claim will processed within a maximum of 6 banking days following the day of receipt of claim i.e. by 9th July.

Reimbursement Authorization vs Reimbursement Undertaking

The difference between a Reimbursement Authorization and a Reimbursement Undertaking are as given below.

URR 725 pdf free download

Please click on the below link to download a copy of URR 725 pdf.

Suggested Readings

- How to clear CDCS Exam

- Back to Back Letter of Credit

- Transferable letter of credit

- What is a Letter of Credit?

- 30 CDCS sample questions with answers

- Disregard, Obligation and Without Delay in UCP 600

- Incoterms 2020 for CDCS exam

- The words Must, May and Should in UCP 600

- What is a Bill of Lading?

- eUCP 2.0 – Uniform Customs and Practice for Documentary Credits for Electronic Presentation Version 2.0

- URR 725 – Uniform Rules for Bank-to-Bank Reimbursements under Documentary Credits

- UCP 600 – Uniform Customs and Practice for Documentary Credits

- SWIFT message types relevant for CDCS Exam

Hi

Unable to download URR725.pdf

Please try now. The link is updated.

Its working now. Thank you.

Hi,

Please clarify.

In your above explanation regarding pre-notification says

“Requirement of a pre-notification of a reimbursement claim should be included by the issuing bank in the reimbursement authorisation and not in the letter of credit.”

But, Article 6f(i) of URR 725 says “pre-notification of a reimbursement claim to the issuing bank must be included in the credit and not in the reimbursement authorization;”

Thanks for highlighting this. The correct statement would be “Requirement of a pre-notification of a reimbursement claim must be included by the issuing bank in the letter of credit and not in the reimbursement authorization.”

A pre-notification of a reimbursement claim is a message sent by the claiming bank to the issuing bank.

A reimbursing bank has nothing to do with this message. So there is no requirement of including this in the reimbursement authorization.

Thank you so much for the clarification. Your blog makes each topic interesting to study.

Thank you. Are you taking the exam?

yes. Taking it on April 16th

All the best for your exam!!

thank you very much. I may bother you with some of my last minute doubts. 🙂

No problem. Hope you have utilized the 3 mock tests.

yet to take the third one. taking it this weekend.

I have a question please

Dose the URR to a letter of credit have any expiration date

I mean if the LC is expired not fully utilized does the URR remain valid even though ?

Thank you

The reimbursement authorization under a letter of credit does not have any expiration date. If LC is expired or not fully utilized, the reimbursement authorization has to be cancelled by sending a message to the reimbursing bank.

Article 7 of URR 725 states that “Except to the extent expressly agreed to by the reimbursing bank, the reimbursement authorization should not be subject to an expiry date…..A reimbursing bank will assume no responsibility for the expiry date of a credit and, if such date is provided in the reimbursement authorization, it will be disregarded.”